Best Practices While Shopping for a Home

Minimize changes and stay in close contact with your loan officer.

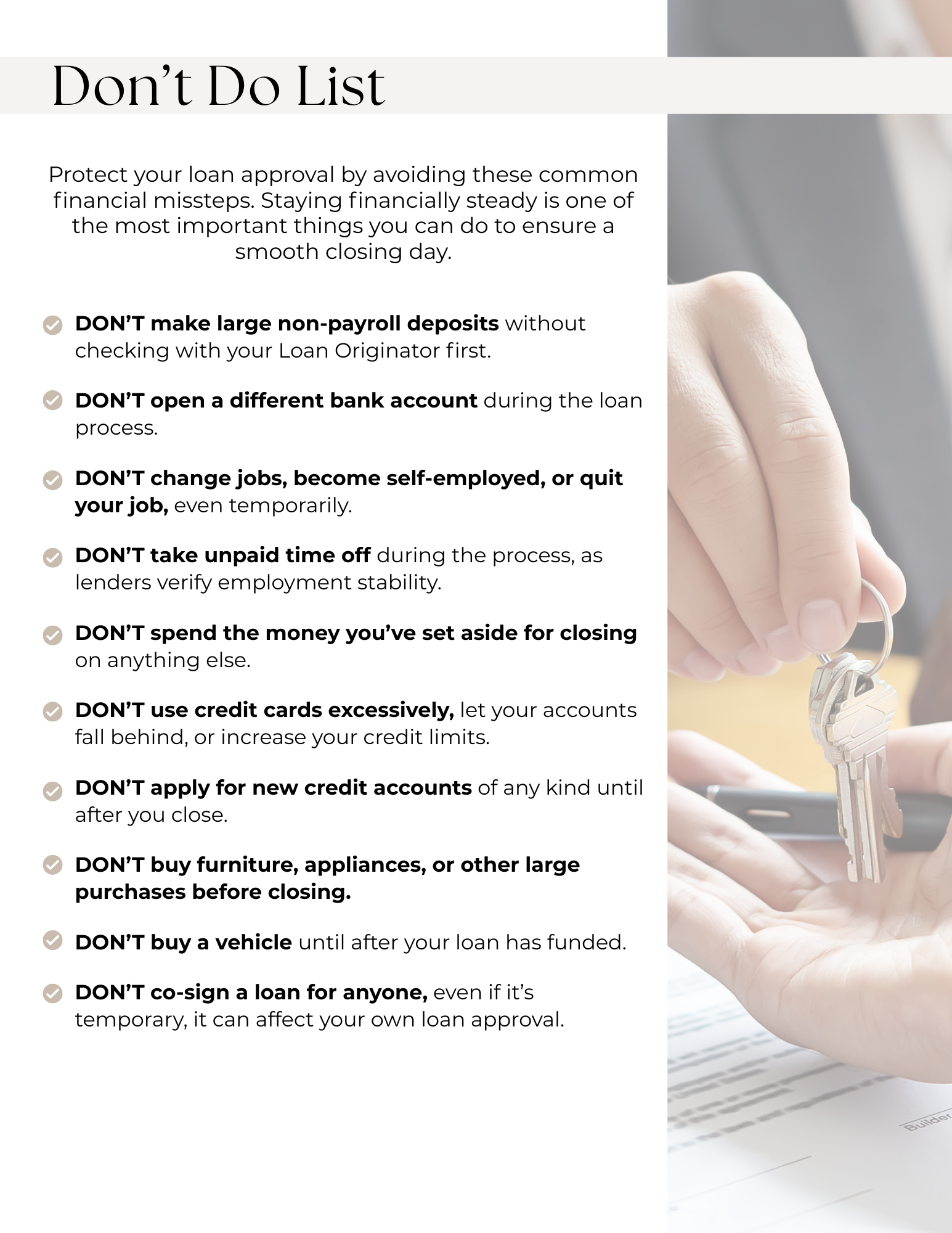

Once you're pre-approved for a mortgage, you’ve cleared an important hurdle in the homebuying process. That pre-approval is based on a snapshot of your financial situation (your credit, income, assets, and debt) at the time of application. While it gives you confidence to shop within a set price range, it's important to understand that your finances will be reviewed again before final approval. That’s why it’s crucial to keep your financial profile stable throughout the process.

Avoid New Debt or Major Financial Changes

Taking on new debt can disrupt your credit profile and jeopardize your mortgage approval. During this time, avoid:

Opening new credit cards or lines of credit

Financing large purchases like furniture, appliances, vehicles, or boats

Co-signing any loans

Running up credit card balances

Missing or making late payments

Even seemingly small changes can raise red flags. Your credit will be pulled again before closing, and any new debt can delay or derail your mortgage approval.

Keep Your Down Payment Clean and Traceable

Your down payment should be in your bank account before you apply, and it needs to come from an acceptable and verifiable source. During the mortgage process:

Avoid making large or unexplained cash deposits

Refrain from opening or closing bank accounts

Only deposit regular, documented income

If you receive a financial gift or have cash on hand, check with your loan officer before depositing it. Any unusual transactions will require explanation and documentation, which can delay the process.

Maintain Job and Income Stability

Stable employment is key to loan approval. While a new job opportunity can be exciting, changing jobs after pre-approval can raise concerns and may require a new approval process or additional waiting time to show income stability.

Keep Communication Open

Your loan officer is your partner throughout the homebuying process. We’ll provide you with a clear list of do’s and don’ts after your pre-approval so you can avoid surprises and keep your transaction on track. If something unexpected comes up, whether it’s a financial change, job update, or a question about next steps, keep us in the loop. Open communication helps us guide you through the process and ensures your pre-approval stays intact.